Incumbent Banks and financial technology startups (Fintechs) face very different challenges as they navigate the COVID-19 crisis. Despite sharing customers and offering similar products, their business models, how they operate, their balance sheets and culture vary tremendously. Each one of these differences impacts how they will perform during and after the crisis.

Banks were already facing challenges: demanding customer expectations, new competitive dynamics, created by low interest rates and even lower barriers to entry for BigTech and Fintechs. Combine these challenges with new regulatory demands from COVID-19 (eased transaction-based commissions, etc.) that highlight the critical role Banks play in supporting small and medium businesses. You have a situation where Banks are being squeezed by economic forces that don’t stand-up in a crisis.

Fintechs have lived a different economic reality. Providing digital-first products and services, Fintechs focus on implementing new technologies and improving customer experience. A sustainable business model comes later. For many of these companies, COVID-19 entered early in their lifecycle. This exposed their vulnerability to economic volatility as growth will stagnate and business models will have to change throughout and after the crisis.

Looking ahead, it’s important to understand the winners and losers - Banks, Fintechs or COVID-19 - as we assess the general impact on the Financial Services industry.

Operational Readiness

Banks have the experience to withstanding a crisis. They have a better understanding of risk and have established processes to deal with massive default, increased regulatory supervision, and unfavorable interest rates. However, this crisis in particular has produced an unseen operational burden brought on by regulators. While this will be the first crisis for most Fintechs, they are built on agile infrastructure and have an ability to manage data that most incumbents lack today.

Banks might have been this before but Fintechs have the ability to make fast changes that level their position.This means they are able to quickly accommodate new regulatory requirements and communicate effectively via digital channels. Overall both are feeling the pain from new operational requirements with no clear end in sight. No winners here.

Winner: COVID-19

Management Effectiveness

While the first priority for all companies has been the well-being of all employees, this has created challenges to preparing the workforce for a new reality, including remote work at scale and the halt to global mobility. Companies have had to quickly adapt existing HR policies, adjust employee contracts, and develop a strategy that ensures continuity of business. Fintechs are uniquely positioned to manage their workforce during the crisis. They are naturally more agile and cloud-based, and experienced with remote work as part of their existing strategy. The learning curve for more established companies is steeper, placing additional pressure on leadership and HR to maintain productivity.

Winner: Fintechs

Financial performance

The business models for Fintechs and Banks differ greatly. Banks operate a positive balance sheet and a portfolio of products generating cash flow. On the other hand, Fintechs operate on the edge of profitability, relying on private capital, with services that limit add-on services (major ones related to travel and FX). Fundraising is likely to be extremely challenging during and after the crisis. Combined with lower consumer spend, both revenue and sustained growth will be greatly pressured. We have started to see this as two of the largest European Fintechs — Monzo and Starling Bank — have furloughed employees and seen upper management take sizable pay cuts.

Winner: Incumbents

Cost Management

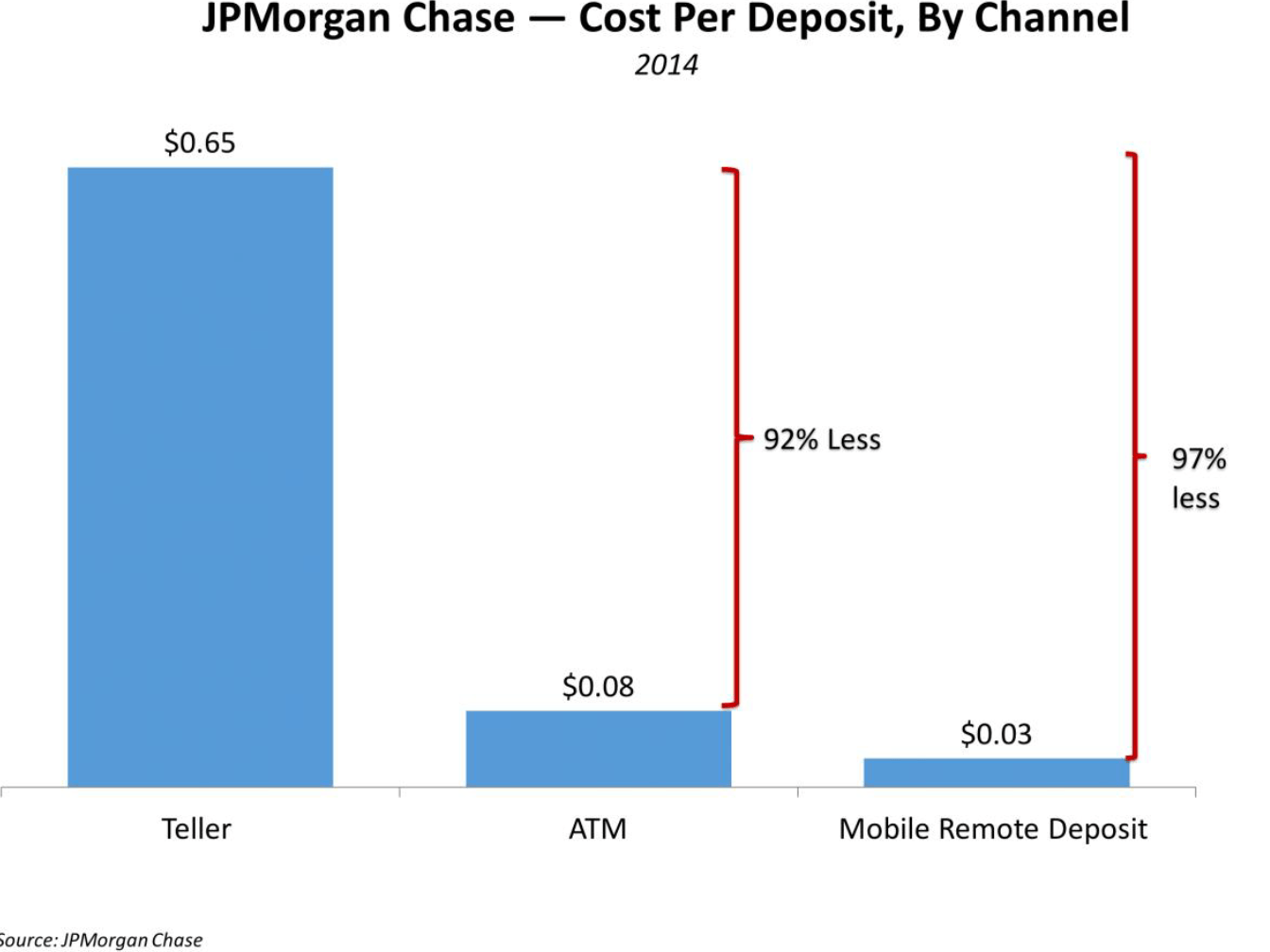

Fintechs that provide 100% digital services have the advantage of operating at a fraction of the cost. Incumbent Banks typically have legacy models that rely on physical branches and support. Both of these models had their advantages/disadvantages pre-COVID. Historically, the digital-focused models have allowed Fintechs to invest their profits into new technology development and partnerships that provide great elasticity and wide margin. An example is N26 who has partnered with Headspace to offer free access to the mental wellness platform to its Metal-tier customers . In the recent past, Banks have made defensive investments in an attempt to keep up with technology demands. Still, legacy infrastructure and data systems are still a reality today. A decade of consumer digital transformation has happened in two months. Banks were left unprepared.

{kind=link}

Winner: Fintechs

Balance Sheet

Capital and liquidity have been challenged as investment continues to decline. The market expects lower prices and fewer rounds while recovering, creating a new level of risk for late-stage Unicorns seeking profitability and/or exit. The effect is that all private companies will have to tighten expenses and make positive cash flow a priority. For startups, the dynamics of balance sheet management, so influenced by investor dollars, has abruptly changed.

How this will impact Fintechs will heavily depend on their stage (later stage will have an easier time) and the risk appetite of the existing investors. Just in the last few weeks, Stripe announced a $600M series G extension at a $36B valuation, Robinhood raised $280M at an $8.3B valuation and N26 raised another $100M in Series D extension. These rounds solidify their investors commitment to the companies despite the current global pandemic. For earlier stage startups, however, the ability to raise will be significantly impacted as the track record and fundamentals aren’t there. This implies lower valuations and a smaller pool of early-stage Fintechs.

Banks will also face balance sheet pressure as liquidity buffers come under pressure from an influx of customers seeking new credit lines and extension of existing ones. This will require careful monitoring and ongoing analysis of deposit fluctuations and capital allocation. Banks are, however, built to manage risk and have developed models that can support them through a crisis. Regulatory bodies have also refined capital requirements over time, ensuring Banks have the tools to withstand an economic downturn.

Winner: Incumbents

Government Assistance

Government programs have been made available to financial institutions to support recovery from COVID-19. To mitigate risk, these programs require a traditional banking license and credit program. The reality is that several Fintechs are not traditional financial services. Many continue to operate under a payments license or an alternative-banking license, that limit access to government support.

Major Banks in the United States were able to take advantage of the $659 billion Paycheck Protection Program (PPP). Offering small businesses and nonprofits forgivable loans to pay their employees during the COVID-19 crisis. Banks are built by and for the financial industry. They’re able to adjust their business models to adjust to the times, always supported by the Government. The additional cash flow and risk insulation is a plus in a crisis.

Understanding the scale and abilities of Fintechs to help quickly at scale, the US government began opening the door for Fintechs to participate in COVID-19 relief programs (e.x.:PayPal, Square). Several U.K.-based Fintechs have also banded together to help self-employed workers prove their income so they can be eligible for financial support. Government has recognized that these loans are complex and that the implications go far beyond the short-term. Here, the potential risks created by non-traditional financial services, typically not subject to government support, might be outweighed by their ability to deploy fast and effective support themselves.

Ultimately, everyone is suffering here. Having access to government aid packages is a welcome source of capital to deploy; however, the real risk comes with managing these loans in the long-run and ensuring low default rates. The impact on the global economy will be felt regardless of who deploys the funds and manages the relationship with businesses across the world seeking aid.

Winner: COVID-19

So Who Wins?

It’s hard to ignore the virus impact. Forecasts estimate US GDP plummeting 30% in summer months and the global economy to contract 3% in 2020. We frequently miss the mark and tend to underestimate the impact of potentially disastrous events. What we know is that the success of both Fintechs and Banks will be determined by their operational readiness, financial performance and ability to adapt their strategy to the existing reality.

We also know that life will go on and the disruption created will create winners and losers.

The changes to business models and funding will create tough-times for Fintechs. They ultimately lose here. The lower-barriers to entry will not be so low and the opportunity created by lagging technology programs are being necessarily closed by the incumbents.

Incumbents have the advantage because they get a second chance. Customers trust them, Governments are enabling them, and the situation is forcing modernization. The opportunity is theirs to lose.