As one of the most disruptive industries, fintech has significantly changed the way we interact with financial companies over the past decade and hasn’t stopped there. Each year brings us new innovations designed to meet growing customer expectations. That’s why it’s important for business owners and executives to understand where we are now and where we’re headed with financial technology in order to maintain relevancy and competitiveness. Let’s talk about the top fintech trends that drive the market.

Global Fintech Market Trends

Before diving into specific fintech areas, let’s take a look at the general fintech market trends that are game-changing for the financial technology scene and check some market statistics.

{kind=link}

WEB 3.0 AND BLOCKCHAIN PROVIDE SECURITY AND DECENTRALIZATION

Following lofty promises and ambitious visions of the future of the Internet, Web 3.0 technologies and blockchain exploded worldwide. Сonsumers are increasingly favoring the ownership of digital goods, made possible by non-fungible tokens (NFTs) and cryptocurrencies. Blockchain is exactly the technology that can support the economy of this virtual space by maintaining exceptional security and providing the necessary financial infrastructure. While cryptocurrencies are a means of payment there, NFTs are reliable proof of ownership of a particular digital asset.

Based on the implementation of blockchain, artificial intelligence and machine learning, and the Internet of Things, Web 3.0 offers a high level of decentralization and personalization, providing financial services users with a completely new customer experience. For example, blockchain allows peer-to-peer transactions without financial intermediaries like banks. However, this does not take banks out of a growing trend. The American banking company J.P. Morgan, announced last year the use of blockchain technology in its new Confirm solution, designed to reduce the cost of payments between banking institutions around the world.

So, blockchain is still an integral part of the development of the fintech market. According to Markets and Markets, the fintech blockchain market size is expected to grow from $230.0 million in 2017 to $6,228.2 million by 2023.

ARTIFICIAL INTELLIGENCE MAKES FINANCIAL OPERATIONS SMARTER

Fintech solutions involve a great deal of data, and there’s no better technology to handle all that data than artificial intelligence. Specifically, machine learning. AI helps with a number of areas of fintech, like risk management, fraud prevention, decreasing operating costs through optimization, personalizing the banking experience, and automating workflows for team members and customers.

Artificial intelligence is best used for recognizing patterns in data, and then AI-powered solutions can give suggestions based on findings to help users reduce or optimize their spending. AI allows financial companies to track the financial health of customers by collecting and processing information about their cash accounts, credit accounts and investments to provide customers with relevant and more personalized services. This can be done through tailored budgeting plans and spending analysis.

The Royal Bank of Canada uses the power of AI to improve user experience and deliver new applications to customers faster. RBC’s private AI cloud can analyze millions of data points, accelerating financial forecast analysis and enabling a company to build and deploy AI-powered apps more efficiently. And this is not the only example. According to Mordor Intelligence, AI in the fintech market is expected to grow from $7.91 billion in 2020 to $26.67 billion by 2026.

EMBEDDED FINANCE EXPANDS SERVICES RANGE

Another top fintech trend is embedded finance, which allows financial technologies to be integrated into non-financial products. For example, at checkout on a website, a user could select an option to buy an item in multiple installments. Another application of this is choosing to add on insurance for an item like a car or electronic device at checkout. As a result, this can increase conversions, yield more valuable data, and increases the competitiveness of products.

Solutions such as embedded payments that support instant online purchases, or embedded insurance that allows you to purchase insurance when buying a plane ticket without the need to contact an insurance agent are not a novelty, but a developing area of fintech. For example, the BNPL (buy now, pay later) uptrend, which we will discuss a little later, is also an example of embedded finance. According to Future Market Insights, the embedded finance market was valued at $43 billion in 2021, and it has all chances to reach $248.4 billion in the next 10 years.

Fintech Lending Trends

Loans, financing, and installment payments are a big part of the fintech industry. Digital lending systems have grown more popular these past several years. There are also many opportunities for artificial intelligence and automation to assist here.

One of the main reasons why alternative lending technology is disrupting the market is because it’s more efficient than traditional lending services. Alternative lenders are much more flexible, so they cater to the different needs of clients. For example, while banks typically provide loans for three to five years, alternative lending is short-term and often low in interest.

Fintech lending trends rely heavily on advances in related fields. For example, through the development of open banking, alternative lenders can access existing accounts while analyzing data, and through machine learning, they can determine spending habits and classify risks. For example, using Optical Character Recognition (OCR) solutions with machine learning helps eliminate all the manual work that lenders have to do to review legal documents. OCR solutions allow you to automatically extract the necessary information from documents, making it available for further processing.

PEER-TO-PEER (P2P) LOANS

The most popular forms of alternative lending include credit unions, microlenders, marketplace lending, and P2P (peer-to-peer) lending.

P2P lending is a specific type of alternative lending technology that involves three parties: a borrower, an investor, and a 3rd party platform online. The 3rd party platform provides the basis for the interaction to take place. This allows the investor to lend money to the borrower without intervention from a bank. Peer-to-peer loaning platforms reduce costs since they don’t own the loans themselves and offer more cost-effective solutions.

P2P lending serves both the consumer and business markets. A growing number of small and medium-sized companies, as well as start-ups, is driving demand for this type of lending. For example, UK-based P2P lending provider Capitalise matches business owners with lenders that can provide a business with funds for various purposes, such as buying new premises, expanding staff, and so on. Marketplace lenders connect borrowers with both individual and institutional investors providing more funding options.

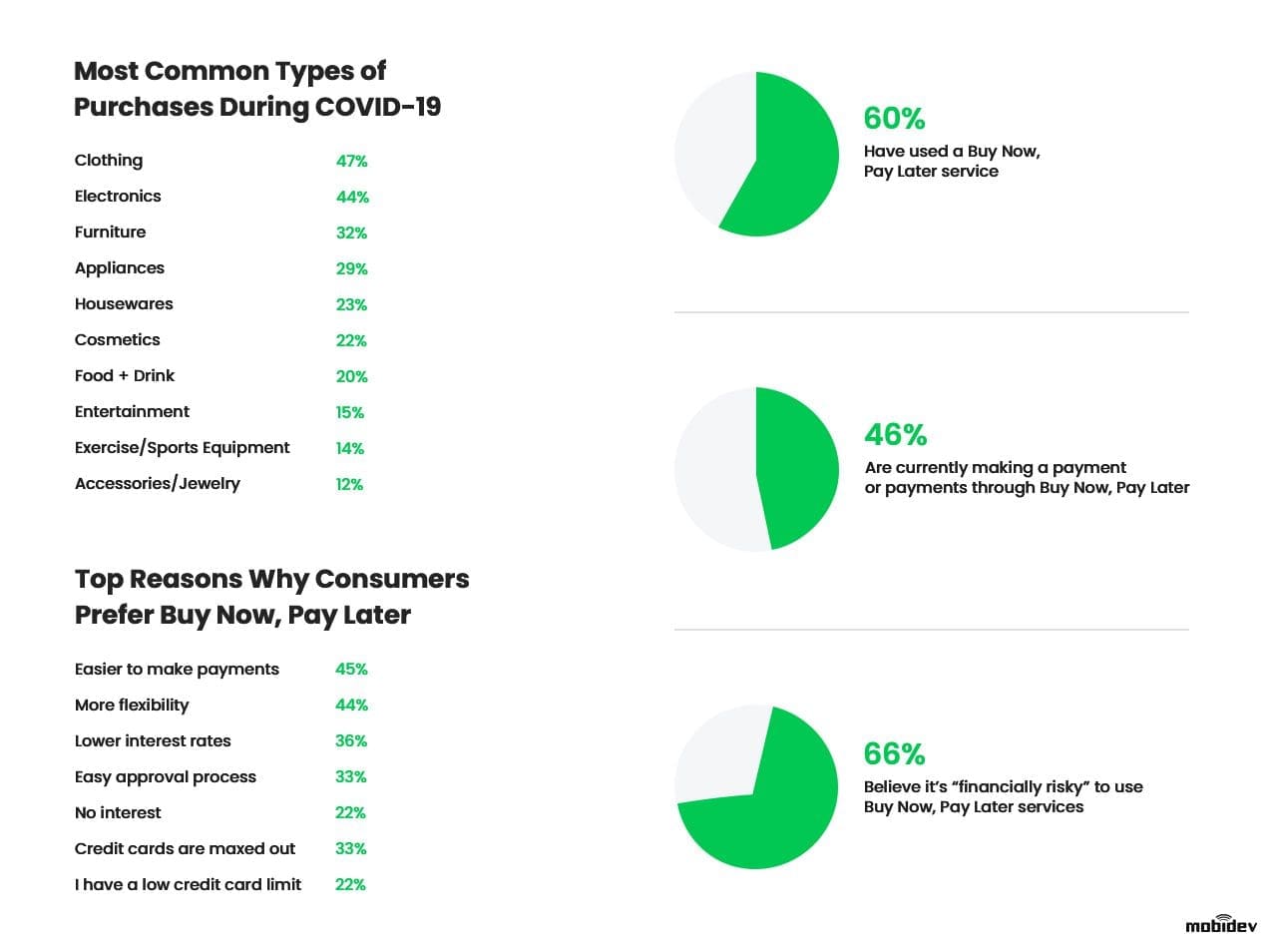

BUY NOW PAY LATER (BNPL)

As an alternative form of short-term financing, Buy Now, Pay Later (BNPL) is a way of paying for products or services later on in the future. Most of the time this works without interest, making it a popular form of financing. With point-of-sale installment loans, customers pay a certain amount down on a purchase and then pay the rest later.

Experts predict a boom in the BNPL sector, and global giants are already following this fintech trend.

For example, Amazon is partnering with Affirm to implement BNPL by splitting purchases of $50 or more into smaller monthly payments.

{kind=link}

Buy Now, Pay Later user habits research by C+R Research

Fintech Payment Trends

Modern payment solutions make it easier for consumers to send and receive money. The expansion of possible payment methods reduces the barriers between the buyer and the company. That’s why when talking about the biggest trends in fintech, we can’t skip a payment area. Let’s dive into it.

CONTACTLESS PAYMENTS ARE ON THE RISE AFTER THE PANDEMIC

No-touch payments have been popular for years after the onset of NFC technologies. Being able to tap a mobile device on a payment terminal not only is simple, but it also helped reduce contact during the COVID-19 pandemic.

Being not new, but easy to adopt, QR code payments are also on the rise. According to Juniper Research, the QR code payment market will be worth $3 trillion by 2025. One of the leaders of this industry is Alipay. Consumers simply need to scan a QR code to direct the app on the device to a page where they can send money securely.

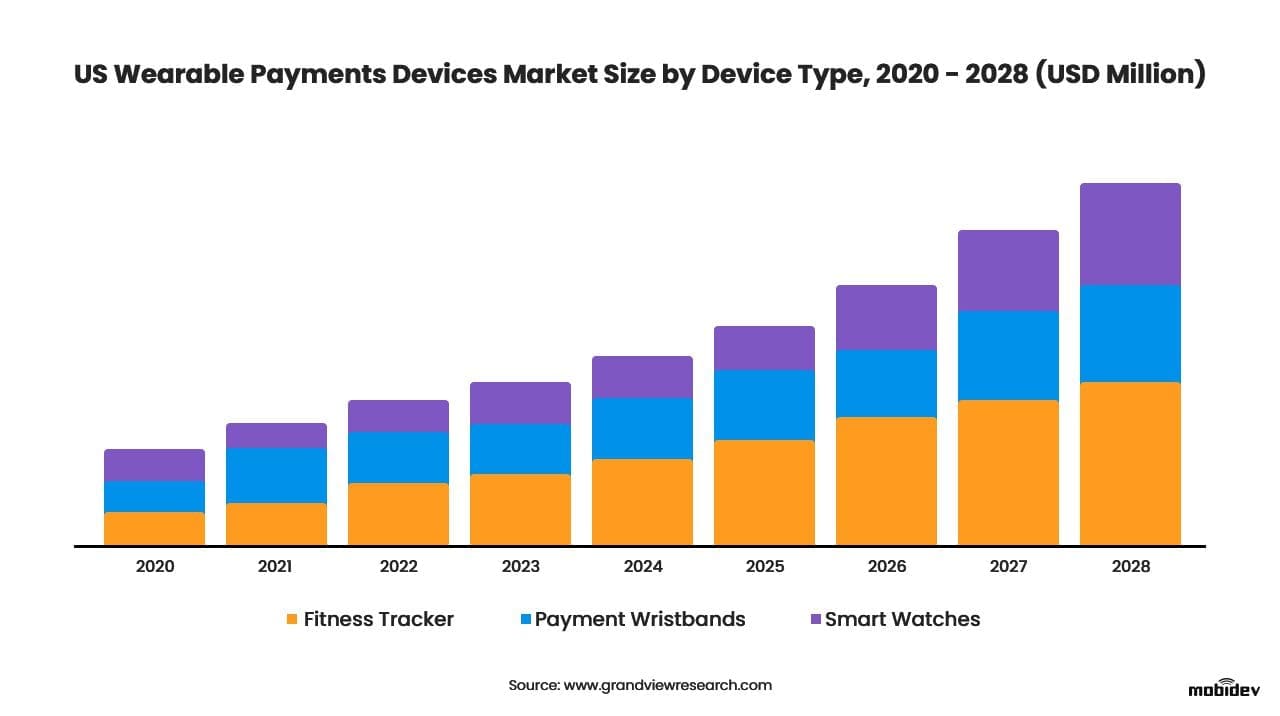

Increasing penetration of NFC and Host Card Emulation (HCE) drives the growth of the wearable payments market. HCE allows wearables, without requiring access to an authentication function, to imitate a card on NFC-enabled devices. Smartwatches aren’t the only wearable with this ability now. Smart NFC rings are also making waves. Innovative hardware like this is proving to be attractive to many consumers.

{kind=link}

REQUEST TO PAY TECHNOLOGY LOWERS TRANSACTION COSTS

This is another trending fintech solution that allows one party to request money from someone else. That person can approve the payment or they can deny it. If the request is approved, the money is transferred in real-time to the recipient. One example of this technology is Zelle, which has partnered with several banks like Huntington.

Request to pay (RTP) technologies are used by consumers, merchants, and businesses that may request bill payments from other businesses. The technology is secure because the payment request is sent to the payer’s proxy billing address without the need to disclose the payer’s sensitive payment details, and the payer has full control over whether to approve or reject the payment. More acquiring and consumer banks are implementing RTP to give businesses real-time visibility into incoming payments while lowering transaction costs.

The request to pay trend originates in the UK where Pay.UK launched it in 2020. Now the technology is gaining momentum around the globe. This is called Request 2 Pay (R2P) in Europe, Request for Payment in the USA and UPI Collect payments in India.

Fintech Banking Trends

Recent years have given us some exciting new trends in fintech that have affected the banking industry. The increased demand for digitalization and the growing adoption of technologies have pushed traditional banks and fintechs to cooperate to jointly develop the market and improve the quality of services.

OPEN BANKING EXPANDS BANK ECOSYSTEM

Banking trends in fintech are largely related to the development of open banking. With the adoption of PSD2 in Europe in 2015, this trend continues to develop rapidly both in the European Union and other regions, opening up a joint development branch of fintech startups and traditional banks.

Open banking is all about sharing financial information in a controlled setting. Account owners can approve ways to securely share their financial information with alternative financial providers. This allows third-party providers to gain access to the customers’ financial information through open APIs. Open banking opportunities are used by many fintech startups that provide budgeting, cost tracking, financial planning, lending and other services. Leveraging open banking APIs will drive the market this year and it’s expected to reach $19.14 billion in 2022, up from $15.13 billion in 2021, according to Business Wire.

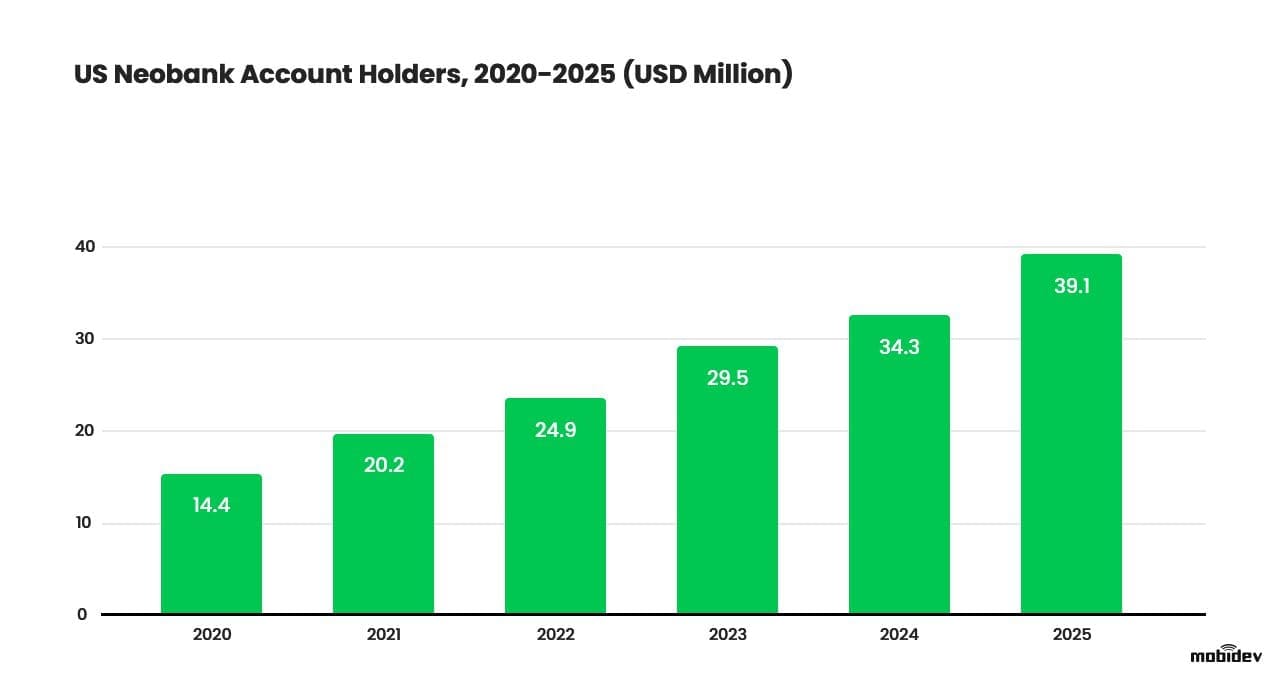

NEOBANKS OFFER MOBILE-FIRST SERVICES AT LOWER COST

Neobanks exist in the fintech space as a way to make banking services more affordable. They generally provide fewer types of services compared to larger banks, but they specialize in these services to improve their quality. Neobanks are also much more transparent about their operations.

Neobanks were also successful due to their valuable features during the COVID-19 pandemic. Instant transfers, fast registration, and IBAN and ACH accounts offered entirely online banking access were beneficial during a time when remote work was a necessity for many industries. Now that the world is recovering from the pandemic, interest in this trend has not faded. Many users have appreciated the advantages of neobanks and are ready to continue to cooperate with them. According to Statista, the number of individuals who hold at least one account at a neobank in the US is expected to peak at 39.1 million in 2025, up from 20 million in 2021.

{kind=link}

BANKING-AS-A-SERVICE ENABLES NEW SOURCES OF GROWTH

This is another important trend in the fintech industry. Banking-as-a-service (BaaS) allows banks to open access to their payment ecosystem to companies that want to provide financial services and build their products on top of traditional banking infrastructure. Thus, non-banks can provide financial services without the need for a banking license, which is very convenient for small businesses who want to get additional profit without investing extra costs in building infrastructure.

BaaS also takes advantage of APIs but unlike open banking, it provides a third party not with ready-made data, but with the functionality of a bank on the basis of which a new product can be developed. Companies pay for access to the BaaS platform, after which the financial institution opens its APIs to that company, providing the systems and information needed to create new financial products.

With the development of interest in BaaS, the list of key market players is growing. Bankable, BBVA, ClearBank, Green Dot., MatchMove Pay Pte., Starling Bank are at the forefront of this fintech area, but new BaaS platforms are popping up all the time, as are a growing number of their users looking to incorporate financial services into their experience. So, we definitely need to keep an eye on this fintech trend to see how it affects the market in the coming years.

Fintech Investment Trends

There are a number of emerging trends in fintech that are changing how investing works. Let’s take a look at the most interesting of them.

CRYPTO ASSETS ARE COMING ALONG WITH THE METAVERSE

Despite the ups and downs of cryptocurrencies in the market, investors continue to include this asset in their portfolios. Therefore, it’s not surprising that trading platforms and crypto exchanges are still gaining popularity in the investment market. With the wide adoption of crypto by companies around the globe, the value of these assets is growing. For example, in June 2022, PayPal announced support for the native transfer of cryptocurrencies between PayPal and other wallets and exchanges, which made this one of the world’s largest payment services crypto-friendly.

However, cryptocurrencies aren’t the full picture. There are also crypto investment opportunities with non-fungible tokens (NFTs). These unique digital items stored on the blockchain, have become quite controversial over the past year due to rampant art theft and misuse. However, NFTs can still be useful as a unique digital license. As long as that license grants the owner access to certain features and items either in digital spaces like video games or in the real world, the token will have use to a user beyond sentimental value.

In fact, digital assets like NFTs and cryptocurrencies are lately associated heavily with the metaverse. As the real world blends further and further with the digital world, investors are increasingly interested in owning digital items that have worth in the digital space. Acquiring metaverse land, purchasing metaverse stocks, investing in metaverse ETFs, and buying NFTs are the most popular ways to invest in the metaverse, a trend that investment platforms are trying to adopt. For example, crypto exchange Coinbase recently announced the development of a unique username NFT that will allow users to carry a unique ID across different worlds in the metaverse. The platform is also working on technology that will allow users to buy avatars for metaverse applications.

ROBO-ADVISORS AND PFMS FOR NOVICE INVESTORS

Thanks to advances in artificial intelligence, automatic financial advice is now a viable solution for many investors. Robo-advisors and personal finance managers (PFMs) use AI suggestions to show optimized ways for investors to spend their money. These kinds of applications are very profitable and are a disruptive force in the market.

Robo-advisors, based on AI data analysis algorithms, are able to process large amounts of data, adapt to a changing landscape faster than human advisors, and offer investors the most appropriate investment options to meet their goals. Since alternative investment tools have significantly lowered the entry threshold for investors and allowed almost anyone to earn money even with small capital, robo-advisors are especially popular among novice investors that don’t have access to traditional consulting.

The Future of the Fintech Industry

As the fintech industry continues to grow, more businesses will get involved in hosting and utilizing solutions like open banking, robo-advisors, BNPL, P2P lending, and more. If we try to find something in common in all fintech trends, then we can identify 3 factors that drive the development of the industry and which must be taken into account by companies wishing to succeed in this area.

- Regulatory compliance. An unexpected hurdle that businesses can face is how governments around the world will catch up with quickly evolving financial industry trends. It’s important for companies to be aware of regulatory changes. Adapting to these changes will be critical for long-term success.

- Blurring of boundaries. As customer expectations rise, the most successful companies are looking to provide more comprehensive services without limits. For example, profitable international payments, the ability to trade crypto, stocks, goods in one application, and so on.

- Increasing accessibility of financial services. Fintech companies strive to make their services for customers as simple and accessible as possible. This includes, for example, simplifying and speeding up the process of buying stocks, quickly calculating interest on a loan, issuing insurance in a few clicks, etc.

Companies that can make progress in these three areas are most likely to be the main market players in the near future.

Written by Maksim Bieliai, Fintech Market Analyst, BA Team Leader at MobiDev.

The full article was originally published here and is based on MobiDev technology research.